Guide to Tax-Saving Investments for FY 2025-26 Under Section 80C

Welcome to our blog on Guide to Tax-Saving Investments for FY 2025-26 Under Section 80C! Section 80C of the Income Tax Act allows you to reduce your taxable income by investing in specific approved instruments, helping you save taxes while securing your financial future. From Employee Provident Fund (EPF), Public Provident Fund (PPF), and National Savings Certificates (NSC) to Equity-Linked Savings Schemes (ELSS) and life insurance premiums, there are multiple ways to make your money work for you. In this guide, we’ll explain each option in simple terms, along with tips on how to maximize your deductions, combine investments, and plan effectively for both short-term and long-term financial goals in FY 2025-26.

Understanding Section 80C: Overview & Benefits

Section 80C of the Income Tax Act is one of the most widely used provisions for reducing taxable income in India. It allows taxpayers to claim a deduction of up to ₹1.5 lakh per financial year on eligible investments and expenses. By investing under Section 80C, you not only lower your tax liability but also build a disciplined approach to saving and wealth creation. This section is especially popular among salaried individuals, self-employed professionals, and small business owners who want to optimize their finances while securing their future. With the right planning, Section 80C can help you achieve both short-term and long-term financial goals.

The benefits of investing under Section 80C are numerous, making it a smart choice for long-term financial planning. Key advantages include:

Tax Savings: Reduce your taxable income by up to ₹1.5 lakh annually, which can lead to significant savings depending on your tax bracket.

Wealth Creation: Investments such as PPF, ELSS, and NSC not only save taxes but also help grow your money over time through compounding.

Financial Security: Life insurance, pension schemes, and other options provide protection for you and your family in case of emergencies.

Encourages Savings Discipline: Regular contributions towards these instruments instill financial discipline and help in consistent wealth accumulation.

Flexibility: With multiple investment options available, you can choose based on your risk appetite, investment horizon, and financial goals.

Combining Investments: You can mix and match instruments like ELSS, PPF, and life insurance to maximize deductions while diversifying your portfolio.

How Much Can You Invest Under Section 80C?

Under Section 80C of the Income Tax Act, you can claim a maximum deduction of ₹1.5 lakh per financial year on eligible investments and expenses. This limit is cumulative, which means all your investments—such as PPF, ELSS, NSC, life insurance premiums, tuition fees, and more—are added together to calculate the total deduction. It’s important to plan how you allocate your funds across these options to make the most of the available tax benefits.

Proper planning ensures that you not only maximize your tax savings but also achieve a balanced investment portfolio that meets your short-term and long-term financial goals. For instance, combining safer options like PPF or NSC with higher-return instruments like ELSS can provide both security and growth while staying within the ₹1.5 lakh limit. Remember, careful planning and timely investments are the key to fully leveraging Section 80C for FY 2025-26.

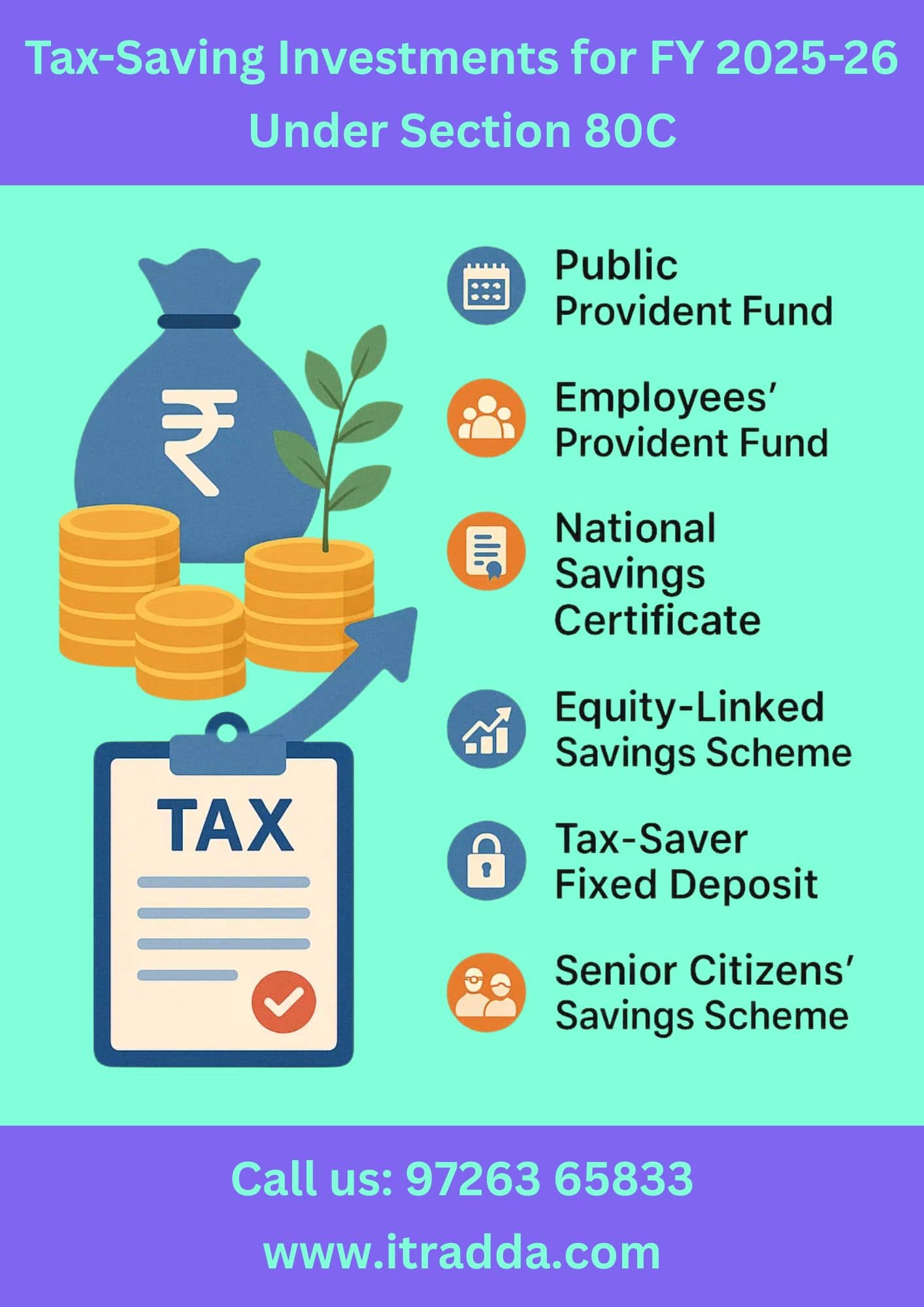

Popular Investment Options for Tax Saving

Section 80C offers a variety of investment options that not only help you save taxes but also grow your wealth over time. Some of the most popular instruments include:

Life Insurance Premiums: Provides financial protection for your family while qualifying for tax deduction.

Public Provident Fund (PPF): A safe, long-term savings option with attractive interest and tax-free returns.

National Savings Certificates (NSC): Government-backed, low-risk investment suitable for fixed-income savings.

Equity-Linked Savings Scheme (ELSS): Mutual funds with higher returns and a short lock-in period of 3 years.

Sukanya Samriddhi Yojana (SSY): A savings scheme for the girl child with tax benefits and guaranteed returns.

Home Loan Principal Repayment: Repayment of the principal amount of a home loan also qualifies under Section 80C.

Eligibility Criteria for Section 80C Investments

To claim deductions under Section 80C, certain eligibility requirements must be met to ensure you get the maximum tax benefit. Here’s a breakdown:

Who Can Claim: Both individuals and Hindu Undivided Families (HUFs) are eligible to claim deductions under Section 80C.

Eligible Investments: Only investments and expenses specified under Section 80C qualify, such as PPF, ELSS, NSC, life insurance premiums, tuition fees for children, and home loan principal repayment.

Investment Period: Investments must be made within the financial year for which you want to claim the deduction. Contributions outside this period will not be eligible.

Documentation: Maintain proper receipts, certificates, and proofs of all eligible investments, as these are required during Income Tax Return (ITR) filing. This includes bank statements, insurance premium receipts, ELSS statements, and tuition fee bills.

Deduction Limit: The total deduction claimed under Section 80C cannot exceed ₹1.5 lakh per financial year, no matter how many eligible investments you make.

Tax Benefits and Limits of Section 80C Investments

Section 80C is one of the most effective ways to save taxes while building your financial future. Here’s everything you need to know in simple terms:

Maximum Deduction: You can claim a deduction of up to ₹1.5 lakh per financial year on eligible investments and expenses. This means your taxable income reduces, lowering your overall tax liability.

Cumulative Limit: The ₹1.5 lakh limit is combined across all Section 80C investments, so planning how much to invest in each instrument is essential to fully utilize the benefit.

Tax-Free Maturity Proceeds: Investments like PPF, ELSS, and Sukanya Samriddhi Yojana not only give upfront tax deductions but also offer tax-free returns on maturity, increasing your overall savings.

Insurance Benefits: Life insurance premiums qualify for deductions while also providing financial protection for your family, ensuring security in case of emergencies.

Home Loan Principal Repayment: Repaying the principal portion of a home loan counts under 80C, helping you save on taxes while building your home equity.

No Carry Forward: Any unused portion of the ₹1.5 lakh limit cannot be carried forward to the next financial year, so it’s important to plan and invest in time.

Combining Investments: Using a mix of safe instruments (like PPF, NSC) and growth-oriented options (like ELSS) can help maximize tax benefits, balance risk, and achieve both short-term and long-term financial goals.

Encourages Financial Discipline: Regular investments under Section 80C help inculcate the habit of disciplined saving and planning for the future.

Choosing the Right Investment According to Your Goals

Selecting the right Section 80C investments starts with understanding your financial goals and risk tolerance. If your aim is long-term wealth creation, instruments like PPF and ELSS are ideal because they offer growth over time while also giving tax benefits. On the other hand, if your priority is securing your family’s future, life insurance provides both protection and tax savings. By knowing your goals, you can pick the investments that serve both your short-term needs and long-term plans.

It’s also important to maintain a balanced portfolio. Combining safer options like PPF or NSC with higher-return options like ELSS allows you to manage risk while maximizing returns. This approach ensures that you get the best of both worlds—financial growth and tax savings. With careful planning and the right mix of investments, you can make the most of Section 80C and build a strong foundation for your financial future.

Common Errors to Avoid When Claiming Section 80C Deductions

Exceeding the ₹1.5 lakh limit

Missing investment deadlines within the financial year

Not maintaining receipts, certificates, or proofs of investment

Ignoring lock-in periods of instruments like ELSS or PPF

Relying on a single investment type instead of diversifying

Overlooking eligibility criteria for Section 80C investments

Investing without aligning to your financial goals

Not reviewing previous year’s investments to avoid repetition

Delaying investments until the last month of the financial year

Assuming all investments automatically qualify without checking rules

Combining Section 80C with Other Tax-Saving Sections

To make the most of your tax-saving opportunities, it’s smart to combine Section 80C with other sections of the Income Tax Act. For example, Section 80D allows deductions on health insurance premiums, Section 80E covers education loan interest, and Section 80G provides benefits for donations to eligible charitable organizations. By strategically planning your investments and expenses across these sections, you can significantly reduce your overall tax liability for FY 2025-26.

At itradda.com, you can find detailed guidance on how to optimize deductions across different sections to save maximum tax legally. For instance, if you invest ₹1.5 lakh under Section 80C, pay ₹30,000 for health insurance under 80D, and claim ₹10,000 in donations under 80G, you could potentially save ₹40,500–₹45,000 in taxes depending on your income slab. Proper planning, timely investments, and accurate documentation are the keys to hassle-free tax filing and maximum savings.

Your Trusted Consultant for Tax Planning and Section 80C Investments

Planning your taxes and choosing the right Section 80C investments can be overwhelming, especially if you are unsure about which options to pick or how to maximize your deductions. Professional guidance can make this process easier, save time, and ensure you get the full tax benefits. Trusted experts at itradda.com help you select the best investment options, organize your documents, and plan your finances effectively for FY 2025-26.

With expert support, you can avoid mistakes, utilize the full ₹1.5 lakh Section 80C deduction, and even combine it with other sections like 80D, 80E, and 80G to maximize tax savings. itradda.com provides reliable advice for salaried individuals, self-employed professionals, and small business owners, ensuring your tax planning is smooth and efficient. For guidance, visit itradda.com or call +91 97263 65833.