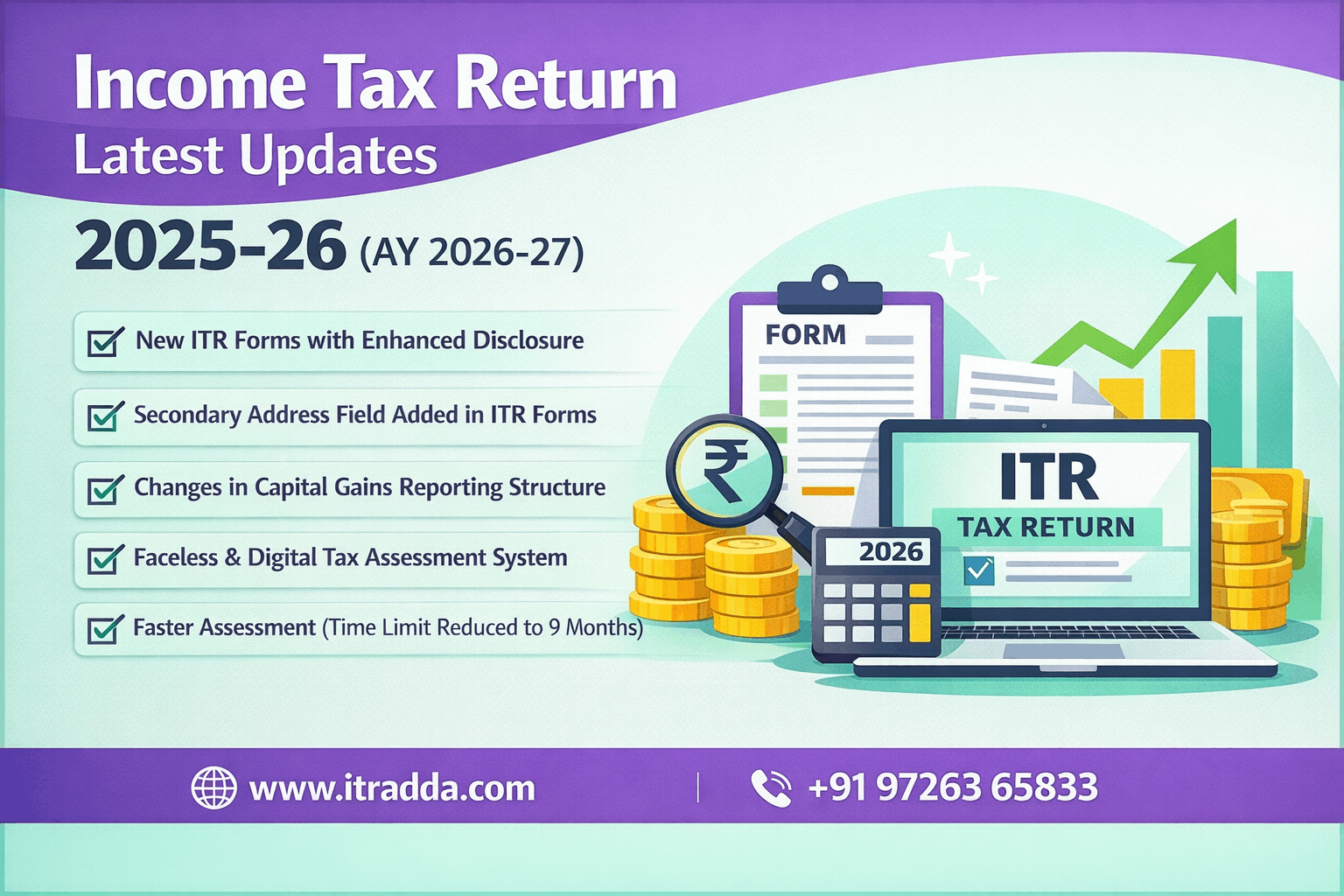

Income Tax Return Latest Updates 2025-26 (AY 2026-27)

The government has proposed the new Income Tax Act, 2025, which is expected to be implemented from 1 April 2026, replacing the existing Income Tax Act, 1961. This update is aimed at simplifying tax laws by using clearer and more structured language, making it easier for taxpayers to understand and comply with the provisions. The new framework is being designed to remove outdated provisions, reduce complexity, and bring more clarity in tax calculations, deductions, and reporting requirements.

Another important aspect of this reform is its focus on a more digital and efficient tax system. With increased use of technology, data integration, and automated processes, the new Act aims to improve transparency and reduce the chances of errors and disputes. It is also expected to strengthen compliance by making reporting more accurate and streamlined. This change is likely to impact the overall return filing process in the coming years, so taxpayers should stay informed and be prepared for these upcoming changes.

View Income Tax Act Details

For AY 2026-27, the new tax regime continues as the default option and has been further improved to make it more beneficial for taxpayers. One of the key updates is the increase in the basic exemption limit to ₹4,00,000, along with a higher rebate under Section 87A of up to ₹60,000. Due to these changes, individuals with income up to ₹12 lakh may effectively have zero tax liability, subject to specified conditions.

The government aims to encourage more taxpayers to shift towards the new regime by offering lower tax rates and simplified compliance without multiple deductions. However, individuals should still compare both regimes before filing their Income Tax Return.

1. Tightened Eligibility for ITR-1 & ITR-4

For AY 2026-27, the Income Tax Department has further tightened the eligibility criteria for simpler ITR forms like ITR-1 and ITR-4 to ensure accurate and complete reporting of income.

2. Foreign Assets & Income Restriction

Taxpayers holding foreign assets or earning foreign income are no longer eligible to file using ITR-1 or ITR-4 and must use detailed forms such as ITR-2 or ITR-3.

3. Multiple Income Sources & Capital Gains

Individuals with overseas income, capital gains, or multiple income sources are required to select appropriate detailed ITR forms based on their income type.

4. Business & Professional Income

Taxpayers engaged in business or professional activities, including F&O trading, must generally file ITR-3 instead of simpler forms.

5. Improved Data Accuracy & Transparency

The updated rules aim to improve data accuracy, transparency, and proper classification of income across different taxpayer categories.

6. Alignment with AIS & TIS

There is increased alignment with AIS (Annual Information Statement) and TIS (Taxpayer Information Summary), making correct form selection more important to avoid mismatches.

7. Stronger Validation System

Enhanced validation systems now check eligibility more strictly, reducing chances of incorrect filing.

8. Consequences of Incorrect Filing

Filing an incorrect ITR form may lead to defective return notices under Section 139(9), delays in processing, or rejection of the return.

9. Faster Processing & Refunds

Correct form selection also helps in faster processing of returns and quicker refunds.

10. Review Before Filing

Taxpayers should review their income sources, disclosures, and financial details carefully before choosing the applicable ITR form.

11. Importance of Correct ITR Selection

These latest updates highlight the importance of selecting the right ITR form to ensure smooth, error-free, and compliant income tax filing.

Form & Income Reporting Errors

- Selecting the wrong ITR form: May lead to defective return or rejection.

- Not reporting all income sources: Interest, freelance, capital gains, etc.

- Incorrect reporting of capital gains: May trigger scrutiny.

- Ignoring foreign income/assets: Can attract heavy penalties.

- Improper F&O turnover calculation: Affects audit applicability.

Mismatch & Validation Issues

- Mismatch with AIS, TIS, 26AS: Can trigger notices.

- Not reviewing pre-filled data: May lead to incorrect filing.

- Mismatch in personal details: PAN, Aadhaar errors cause issues.

- Not disclosing high-value transactions: Must be reported properly.

Filing & Compliance Mistakes

- Filing at the last minute: Leads to errors and technical issues.

- Not verifying return: Makes return invalid.

- Skipping tax payment: Results in interest and penalties.

Documentation & Financial Errors

- Claiming incorrect deductions: May lead to disallowance.

- Incorrect bank details: Delays refunds.

- Not maintaining documents: Causes issues during assessment.

Original Return

31 July 2026 – Salaried individuals (ITR-1, ITR-2)

31 August 2026 – Business/professional taxpayers (ITR-3, ITR-4 – non-audit)

👉 Additional time for business taxpayers

Belated Return

31 December 2026

Applicable if deadline is missed with late fees and interest

Revised Return

31 March 2027

👉 More time to correct errors or omissions

Key Highlights

- Deadlines based on taxpayer category

- More time for accurate filing

- Stronger validation system

Important Points

- Penalty up to ₹5,000 + interest

- Late filing may delay refunds

- Early filing avoids last-minute issues